The American clothing manufacturing industry has experienced a dramatic transformation over the past several decades. Once a thriving sector that employed millions, the rise of globalization, outsourcing, and changing consumer preferences have contributed to its significant decline. The proliferation of fast fashion and free trade agreements have further accelerated this shift, making it increasingly difficult for domestic manufacturers to compete.

Despite these challenges, a resurgence in interest in ethically produced, high-quality, and sustainable clothing has begun to shift the narrative. Consumers are increasingly demanding transparency, fair labor practices, and environmentally friendly production methods. This research paper explores the state of American clothing manufacturing, examining historical and current trends, employment shifts, the impact of trade policies, and the evolving consumer sentiment toward domestically produced apparel.

In a Nutshell

- Over 97% of clothing sold in the U.S. is imported, with China, Vietnam, Bangladesh, and India being the top sources.

- Only 2.5% of apparel purchased in the U.S. is domestically produced, highlighting the dominance of offshore manufacturing.

- American apparel manufacturing jobs have declined sharply, from over 900,000 in 1990 to fewer than 100,000 today.

- The number of U.S. apparel manufacturers has significantly decreased, falling from 15,478 in 2001 to approximately 7,000 in recent years.

- The de minimis loophole allows foreign sellers to ship products duty-free directly to U.S. consumers, giving overseas manufacturers and e-commerce giants like Shein and Temu a competitive advantage.

- Consumer sentiment toward American-made clothing remains strong, with surveys indicating that 78% of Americans prefer to buy domestically made apparel when given the choice, though price remains a major barrier.

- Fast fashion has further driven offshoring as brands prioritize low costs and high-speed production over domestic manufacturing.

- Reshoring efforts, automation, and sustainability initiatives are creating new opportunities for the industry, but scaling these efforts remains challenging.

- Legislative efforts, such as the Import Security and Fairness Act, aim to close trade loopholes and provide incentives for domestic production.

- The future of American apparel manufacturing depends on a combination of policy changes, consumer behavior, and technological advancements to ensure long-term viability.

Our Methodology

This research is based on a combination of government reports, industry analyses, consumer surveys, and direct case studies. Primary data sources include:

- The Bureau of Labor Statistics (BLS)

- The U.S. Census Bureau

- The Office of Textiles and Apparel (OTEXA)

- Industry trade associations such as the National Council of Textile Organizations (NCTO)

We have also gathered data from consumer sentiment surveys and analyzed key trends from major apparel brands that still manufacture in the U.S.

American Clothing Manufacturing Trends

Historically, the United States was a global leader in clothing production, with cities like New York, Los Angeles, and Chicago serving as hubs for textile and garment manufacturing. However, the industry began to decline in the latter half of the 20th century as trade agreements opened the U.S. market to lower-cost imports. The introduction of the North American Free Trade Agreement (NAFTA) in 1994 and China’s entry into the World Trade Organization (WTO) in 2001 significantly accelerated this decline.

According to data from OTEXA, U.S. textile and apparel production has declined by over 80% since the 1980s. The rise of fast fashion brands like Zara and H&M has exacerbated this trend by prioritizing speed and cost over quality and sustainability. While domestic brands such as American Giant and Todd Shelton have carved out niche markets by emphasizing durability and ethical production, they remain exceptions rather than the norm.

The Decline In The Number of U.S. Apparel Manufacturers (2001-Present)

Over the past two decades, one of the most striking trends in American clothing manufacturing has been the sharp decline in the number of apparel manufacturers operating in the United States. According to data from the Bureau of Labor Statistics’ Quarterly Census of Employment and Wages (QCEW), the number of apparel manufacturing establishments has decreased significantly since the early 2000s.

The table below illustrates this trend by presenting the number of apparel manufacturers in the U.S. from 2001 onward. This decline reflects the broader shifts in the industry, including offshoring, increased reliance on imported goods, and the challenges faced by domestic manufacturers in competing with lower-cost production overseas.

Several key factors have contributed to this decline:

- Global Trade Agreements: The expansion of trade agreements such as NAFTA and China’s entry into the World Trade Organization in 2001 accelerated the movement of apparel production to lower-cost countries.

- Labor Costs: U.S. labor costs are significantly higher than those in major apparel-exporting countries like China, Bangladesh, and Vietnam.

- Supply Chain Consolidation: As major retailers sought to streamline their supply chains, many domestic manufacturers were squeezed out in favor of large overseas factories that could produce goods at scale.

- Fast Fashion Growth: The rise of fast fashion brands like H&M, Zara, and Shein has placed increased pressure on manufacturers to produce at low costs and high volumes—an environment that has been difficult for American manufacturers to compete in.

Despite these challenges, some manufacturers have been able to survive by specializing in high-quality, small-batch production, sustainable apparel, and niche markets such as workwear and military uniforms. Recent trends toward reshoring, sustainability, and automation suggest that this decline could stabilize or even reverse in the coming years.

The following table presents the number of apparel manufacturers in the U.S. from 2001 to the most recent available data:

| Year | Number of Manufacturers |

|---|---|

| 2001 | 15,478 |

| 2002 | 14,182 |

| 2003 | 13,391 |

| 2004 | 12,360 |

| 2005 | 11,264 |

| 2006 | 10,950 |

| 2007 | 9,492 |

| 2008 | 9,033 |

| 2009 | 8,339 |

| 2010 | 7,855 |

| 2011 | 7,367 |

| 2012 | 7,221 |

| 2013 | 7,058 |

| 2014 | 7,031 |

| 2015 | 6,940 |

| 2016 | 6,787 |

| 2017 | 6,685 |

| 2018 | 6,789 |

| 2019 | 6,653 |

| 2020 | 6,418 |

| 2021 | 6,398 |

| 2022 | 6,568 |

| 2023 | 6,546 |

Source: BLS.gov

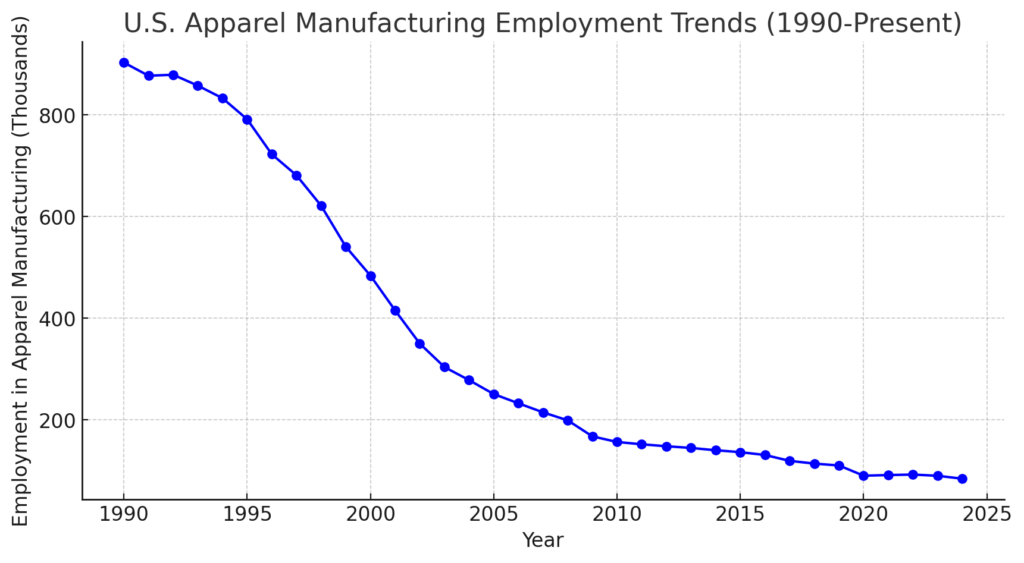

American Clothing Employment Trends

Employment in the American clothing manufacturing sector has been on a continuous downward trajectory.

- In 1990, over 900,000 Americans worked in apparel manufacturing.

- By 2023, that number had dwindled to fewer than 100,000, according to BLS data.

The decline in jobs has had widespread consequences, particularly in regions that were once manufacturing strongholds, such as North Carolina, South Carolina, and California.

Source: BLS.gov

The primary reason for this decline is the cost differential between American and overseas labor, which is a common theme across all manufacturing industries. While the average hourly wage for an American apparel worker is approximately $15-$20, workers in Bangladesh and Vietnam often earn less than $1 per hour. This wage gap, combined with lower regulatory costs abroad, has incentivized companies to offshore production.

How Much of The Clothing Sold In The U.S. Is Made In The U.S.?

According to OTEXA, only about 2.5% of apparel purchased in the U.S. is domestically produced. The overwhelming majority of clothing is imported, primarily from China, Vietnam, Bangladesh, and India.

Here’s a detailed breakdown of the top countries from which the United States imports apparel:

| Country | Import Value (US$ Million) | Percentage of Total U.S. Apparel Imports |

|---|---|---|

| China | 27,000 | 27.0% |

| Vietnam | 14,000 | 14.0% |

| Bangladesh | 9,000 | 9.0% |

| India | 8,000 | 8.0% |

| Mexico | 5,000 | 5.0% |

| Indonesia | 4,500 | 4.5% |

| Honduras | 3,500 | 3.5% |

| Cambodia | 3,000 | 3.0% |

| Pakistan | 2,500 | 2.5% |

| Italy | 2,000 | 2.0% |

Note: The import values are approximate and rounded to the nearest hundred million.

This data illustrates that China remains the leading source of apparel imports for the U.S., accounting for approximately 27% of total imports. Vietnam and Bangladesh follow, contributing 14% and 9% respectively. Collectively, these top 10 countries account for about 78% of all U.S. apparel imports.

American Sentiment For Buying American-Made Clothing

Despite the overwhelming presence of imported clothing, consumer sentiment toward American-made apparel remains strong.

A 2023 survey conducted by the Reshoring Institute found that:

- 78% of American consumers prefer to buy domestically produced clothing when given the choice.

- 62% cited price as a primary deterrent.

A 2023 report by Morning Consult revealed that nearly two-thirds of U.S. consumers actively sought “Made in America” products over the past year. However, while many are willing to pay a premium for domestically produced goods, the majority are hesitant to pay more than 10% above the price of foreign-made equivalents. This price sensitivity underscores the importance of competitive pricing for American manufacturers.

Demographic Factors

Demographic factors also significantly influence purchasing decisions. The same Morning Consult report found that Republicans and Baby Boomers are more inclined to seek out American-made products than Democrats and younger generations. This suggests that marketing strategies emphasizing national pride and economic patriotism may resonate more with certain segments of the population.

Impact of Policy Changes

Recent policy changes may further impact consumer behavior. For instance, the imposition of a 10% additional tariff on Chinese imports in early 2025 is expected to lead to price increases and shipping delays for foreign-produced apparel. Experts anticipate that these developments could shift consumer preferences toward American-made products as a means to avoid tariff-related costs and support local businesses.

Price Sensitivity Is Still The Biggest Driver of Behavior

While American consumers strongly prefer domestically produced apparel, purchasing decisions are influenced by price sensitivity, demographic factors, and market availability. Ongoing economic and policy developments may further shape these behaviors, presenting both challenges and opportunities for American clothing manufacturers.

Policy and Trade Considerations

One of the biggest policy issues affecting American clothing manufacturing is the de minimis loophole, which allows foreign sellers to ship products directly to U.S. consumers without paying duties or tariffs if the shipment is valued under $800. This has given an enormous competitive advantage to foreign brands, particularly Chinese e-commerce giants like Shein and Temu.

Legislative Efforts to Address the De Minimis Loophole

Several legislative proposals have been introduced to address the impact of the de minimis loophole on American manufacturers.

Import Security and Fairness Act

This bill, introduced in the U.S. House of Representatives, aims to close the de minimis loophole for shipments originating from non-market economies such as China. The legislation proposes increasing oversight on high-volume shippers, ensuring e-commerce platforms like Shein and Temu do not exploit de minimis rules to bypass tariffs and import regulations.

End China’s De Minimis Abuse Act

This Act directly targets Chinese e-commerce firms that use de minimis loopholes to flood the U.S. market with ultra-cheap goods. The bill seeks to curb the flow of de minimis shipments from China into the U.S. by eliminating the use of de minimis for goods subject to Section 301 tariffs or other U.S. trade remedies.

Other Tariff Reform Legislation

There are several pieces of legislation on the table focused on reducing tariff disparities that penalize American manufacturers. They call for a review of the tariff structure that disproportionately taxes American-made goods while allowing foreign-made products to enter at a lower rate.

The Future of American Clothing Manufacturing

The future of American clothing manufacturing is poised at a critical juncture, shaped by evolving consumer preferences, technological advancements, sustainability efforts, and potential policy changes. While challenges such as high labor costs and global competition remain, several key trends suggest opportunities for revitalizing domestic apparel production.

The Role of Automation and Robotics

One of the most significant factors shaping the future of American clothing manufacturing is the increasing adoption of automation and robotics. Technologies such as AI-driven sewing machines, 3D knitting, and robotic cutting systems are revolutionizing the production process. Companies like SoftWear Automation are developing autonomous sewing systems that can dramatically reduce labor costs and improve efficiency. If widely adopted, these innovations could help U.S. manufacturers compete with low-wage foreign labor markets while maintaining high-quality production standards.

Reshoring and Nearshoring Initiatives

Over the past few years, many companies have begun reshoring some of their manufacturing operations to the U.S. due to supply chain disruptions, increased shipping costs, and growing consumer preference for American-made products. Nearshoring, where companies shift production to closer locations like Mexico and Central America, is also gaining traction as a compromise between cost-effectiveness and logistical efficiency.

A 2023 report from the Reshoring Institute found that 62% of surveyed companies were considering reshoring or nearshoring their production due to rising costs in China and increased global instability. As transportation costs continue to rise and geopolitical tensions impact supply chains, more American companies may look to bring production back closer to home.

The Growing Demand For Sustainable and Ethical Manufacturing

Sustainability is an increasingly important factor in consumer purchasing decisions. The apparel industry is one of the largest contributors to global pollution, and growing awareness of its environmental impact has led to a shift in demand for sustainable alternatives.

Many American brands are responding by investing in organic cotton, recycled materials, and eco-friendly dyes, as well as adopting circular economy practices, such as textile recycling and take-back programs. Companies like Patagonia and Reformation have built their reputations on sustainable practices, and as consumer awareness continues to rise, more domestic manufacturers will likely follow suit.

Additionally, government incentives could play a role in supporting sustainable manufacturing. Proposed policies that offer tax credits for sustainable production, grants for green technology investments, and stricter environmental regulations on imported goods may encourage more companies to manufacture responsibly within the U.S.

The Impact of Policy Changes and Trade Regulations

Government policies will play a crucial role in shaping the future of domestic apparel manufacturing. Several legislative efforts, including those aimed at reforming the de minimis loophole, may significantly impact the industry. If laws are enacted to increase tariffs on foreign-made goods or provide incentives for domestic production, we could see a shift in where apparel is manufactured.

Additionally, trade agreements with key allies may facilitate more regional production within North America, particularly through stronger USMCA (United States-Mexico-Canada Agreement) policies that incentivize manufacturers to keep production within these regions.

The Role of Customization and On-Demand Manufacturing

The rise of direct-to-consumer brands and customization technology is changing the way clothing is produced and sold. More consumers are demanding personalized clothing, and advancements in digital textile printing, automated pattern making, and AI-driven customization tools allow manufacturers to produce garments on demand, reducing waste and excess inventory.

Companies like Unspun and Ministry of Supply are leveraging these technologies to create personalized apparel at scale, allowing consumers to receive tailored clothing while keeping production within the U.S. This shift to on-demand manufacturing could reduce dependency on mass production overseas and provide a competitive advantage for domestic manufacturers.

Consumer Trends and The Buy American Movement

A strong “Buy American” sentiment continues to gain traction, driven by both patriotic and ethical considerations. Consumer surveys indicate that more shoppers are willing to pay a premium for U.S.-made clothing, particularly when quality, transparency, and sustainability are emphasized. Brands that effectively market their American-made products with strong storytelling and brand authenticity will likely benefit from this trend.

In response, retailers are adjusting their supply chains to include more American-made goods, and online platforms like us at AllAmerican.org are helping connect consumers with domestic manufacturers. Continued education on the benefits of American-made apparel will further drive demand in the coming years.

Revitalizing American Apparel Manufacturing: The Path Forward

The American clothing manufacturing industry has faced decades of decline, driven by globalization, trade policies, and shifting consumer behavior. The overwhelming reliance on imported apparel has made it difficult for domestic manufacturers to compete, resulting in job losses and a shrinking number of apparel producers. However, the future is not without promise. Several key factors, including reshoring initiatives, advancements in automation, sustainability trends, and evolving trade policies, present opportunities for revitalization.

Challenges and Opportunities

The industry continues to struggle against low-cost foreign competition, supply chain vulnerabilities, and high labor costs. The dominance of fast fashion, the de minimis loophole, and tariff disparities have further hindered domestic manufacturers. However, the growing demand for ethically produced, sustainable, and locally made clothing suggests a shift in consumer preferences that could support American apparel makers willing to adapt.

Government policy will play a crucial role in shaping the industry’s future. Legislative efforts to close trade loopholes, such as the Import Security and Fairness Act, could level the playing field for domestic manufacturers. Meanwhile, incentives for automation, workforce training, and sustainable production can help the industry compete in a modernized global economy.

Key Takeaways For Industry Stakeholders

- Policymakers must prioritize trade reforms, including addressing the de minimis loophole, to prevent unfair advantages for foreign competitors. Support for domestic manufacturers through tax incentives and infrastructure investments is also crucial.

- Manufacturers should embrace automation, invest in sustainable materials, and adapt to new consumer demands for transparency and ethical sourcing.

- Retailers and brands can play a pivotal role by supporting American-made products, reshoring parts of their supply chain, and educating consumers about the benefits of domestically produced apparel.

- Consumers have the power to drive change by making conscious purchasing decisions that support American workers and businesses.

A Vision For The Future

While the road ahead presents challenges, there is potential for a revitalized American apparel manufacturing industry—one that is more sustainable, technologically advanced, and economically viable. With strategic investment, policy support, and a collective shift in priorities, the United States can rebuild a competitive and resilient apparel sector. The key to this resurgence will be collaboration between government, businesses, and consumers, ensuring that “Made in America” is not just a label, but a thriving industry once again.